Modified Duration

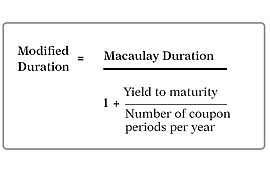

Modified Duration is a metric that measures a bonds sensitivity to changes in yield

- The math behind it is complicated

- The rule of thumb is that duration measures the percentages change in the bonds price for a 1% change of yield

- Can be applied to any income security or security with similar attributes (not just bonds) - REITS, Loans, etc.

Example

- Assume a US Treasury Bond has a Duration of 7.5

- If interest rates move up by 1%, expect the price of the bond to drop by 7.5%

- If interest rates drop by 1%, expect the price of the bond to increase by 7.5%